The Missing Investment in Primary Care

- Primary care is essential but broken: Despite proven links to better outcomes and lower costs, primary care remains underfunded (only 5% of $5T spend) and inaccessible to many (⅓ of Americans lack access).

- Old models are failing: Capital-intensive efforts have shuttered, revealing deep economic and operational flaws in scaling primary care delivery.

- New hope lies in enablement: Investment should shift from building clinics to backing infrastructure—AI tools, workflow automation, and platforms that empower providers, not replace them.

- What’s working: Lightweight, tech-enabled, service-integrated models show real promise by addressing burnout, access, and cost without heavy real estate.

- Investor takeaway: Avoid direct care delivery bets for now—back the “picks and shovels” powering primary care’s rebuild.

Primary care is often described as the “quarterback” of the healthcare system. It is often the first and most consistent touchpoint in a person’s health journey. When patients consistently engage with primary care—particularly for preventative services and chronic care management—it leads to better health outcomes, lower healthcare costs, and fosters more efficient use of the health system’s resources. Yet, despite its critical role, primary care in the United States has traditionally been underfunded and underutilized.

Why Primary Care is Healthcare’s MVP

Primary care encompasses family medicine, internal medicine, pediatrics, geriatrics, and for many women, their OB/GYN. These providers manage the majority of a patient’s health needs, coordinate referrals to specialists, oversee preventative screenings, and manage chronic care conditions. High-quality primary care is longitudinal and comprehensive, addressing the entire person rather than isolated symptoms or episodes.

Robust primary care access is directly correlated with reduced emergency department visits and hospitalizations. In fact, greater access to and utilization in primary care services in a given area is associated with longer life expectancy. Unfortunately, patients without a dedicated primary care provider often experience delayed care or rely on high-cost settings like emergency departments, ultimately inflating medical costs. A 2019 Stanford study found that every 10 additional primary care physicians per 100,000 people was associated with a 51.5-day increase in life expectancy (Stanford Medicine).

A System Under Pressure

Despite representing the backbone of the healthcare system, primary care receives just about 5% of the total $5T annually US healthcare spend (KFF). Nearly one-third of Americans do not have access to a primary care physician (NACHC). Independent PCP practices are vanishing as health systems, payers, and private equity firms acquire them, fundamentally shifting the ownership landscape. In 2012, 60% of primary care physicians owned or worked in independent practices. By 2022, that number had dropped below 47% (AMA). This consolidation often limits physician autonomy, prioritizes financial metrics over patient outcomes, and may create misaligned incentives that undermine the personalized, longitudinal relationships essential to effective primary care.

The chronic underinvestment in primary care has systemic consequences: an overburdened workforce, a shrinking pipeline of future PCPs, and declining patient access. With an anticipated shortage of 17,800 to 48,000 primary care physicians by 2034, access issues will worsen, particularly in rural and underserved areas (HRSA).

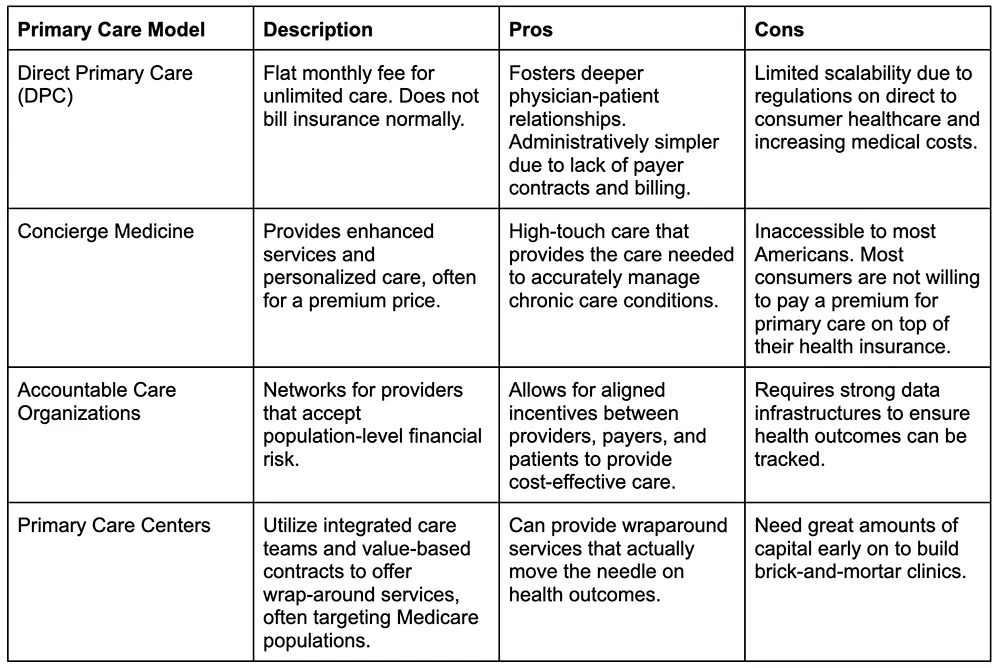

The Rise of Advanced Primary Care Models

To combat these challenges, innovators have created a range of new models that aim to reimagine care delivery.

Investment Trends and Market Dynamics

Over the last decade, primary care and adjacent enablers have attracted billions in venture capital. Digital health funding peaked at $29.1 billion in 2021, with a substantial portion directed toward primary care innovation (Rock Health). Retailers (e.g., CVS, Walgreens), big tech (e.g., Amazon), payers (e.g., Humana, UnitedHealth), and a wave of startups have entered the space. While these moves signal confidence in the value of primary care, they have also revealed its structural fragility.

Retail giants like Walmart and Walgreens have attempted to scale clinic-based models inside their stores. Venture-backed startups such as Forward and Carbon Health have launched concierge-like experiences with strong technology underpinnings. At the same time, MSOs like Aledade and Privia have provided independent practices with tools to transition to value-based care.

Yet despite large capital inflows, few primary care models have delivered scalable, profitable growth. Strategic exits (e.g., One Medical’s acquisition by Amazon) dominate the landscape, and many promising companies struggle to balance care quality with financial sustainability (Fierce Healthcare).

Tailwinds: Reasons for Optimism

Several factors support continued innovation in primary care:

- Policy & Payment Reform: CMS continues to push value-based payment through models like the 2025 Advanced Primary Care Management program. These models provide per-member-per month payments for comprehensive services, helping providers move beyond fee for service (CMS Innovation Center).

- Legislative Support: Bills like H.R. 3029 (see here) and H.R. 3836 (see here) aim to expand DPC’s reach by allowing patients with HSAs or Medicaid to participate—potentially unlocking new demand for membership-based care.

- Demographic Trends: The U.S. population is aging, and chronic diseases are rising. By 2030, more than 20% of Americans will be over 65 (PRB). Effective primary care is essential to managing this shift.

- Technology & AI: Tools that reduce documentation burden (e.g., AI scribes), support virtual triage, or enable better data integration are beginning to enhance provider productivity and reduce burnout. Clinician adoption of such tools are growing (Rock Health). Startups such as Tia are combining AI-driven engagement with personalized clinical care, helping women manage reproductive, mental, and preventative health within a unified platform. Similarly, Summer Health uses lightweight automation and text-first communication to make pediatric care more accessible, while EvolvedMD integrates behavioral health into primary care settings. Models such as these ultimately use technology to enhance the PCP and patient relationship.

Headwinds: Structural and Operational Challenges

Despite these positive signals, the path forward for primary care remains difficult:

- Unsustainable Economics: Primary care is poorly reimbursed—an average PCP visit earns ~ $259, compared to over $1,000 for specialty care. Practices often depend on high patient volume to survive, leading to rushed visits and physician burnout (KFF).

- Workforce Shortages: Burnout is rampant, and primary care is one of the lowest paid specialities. With a looming supply shortage and weak recruitment numbers into the field, scaling primary care capacity remains a challenge (HRSA).

- Payment Transition Friction: Many PCPs are stuck between legacy fee-for-service and emerging value based models, forced to operate both simultaneously. The hybrid model undermines incentives and ultimately complicates their financial forecasting (Milbank Memorial Fund).

- Recent High-Profile Failures: Multi-billion dollar efforts have failed to produce sustainable outcomes. VillageMD (acquired by Walgreens), Walmart Health, and Forward have all pulled back or exited the market entirely. These failures highlight the fragility of capital-intensive care delivery models.

Learning from Failure: A Cautionary Tale

VillageMD (Walgreens) received over $6 billion in investment to build co-located primary care clinics inside Walgreens stores. Despite scale in Texas, patient demands and margins lagged in other states. By 2024, Walgreens slashed its expansion plan and wrote down their investment (AHA).

Walmart Health closed all 51 of its clinics in April 2024. The company cited unsustainable reimbursement rates and rising medical costs. Without hospital revenue or any higher-margin services, Walmart could not cross-subsidize its primary care offering (Walmart).

Forward Health raised $650 million to build futuristic, AI-enabled clinics. Its cash-pay model excluded insurance and specialist referrals, limiting their total addressable market. The company shut down in late 2024 (Fierce Healthcare).

Cano Health, PlushCare, and CareMore’s Aspire Health division have also scaled back or exited their primary care efforts. Even One medical, considered as a success story, never achieved profitability as a public company (Fierce Healthcare).

These cautionary tales show that capital, retail brand recognition, and advanced technology alone cannot solve primary care’s broken economics. Profitability requires careful payer alignment, patient engagement, and cost control.

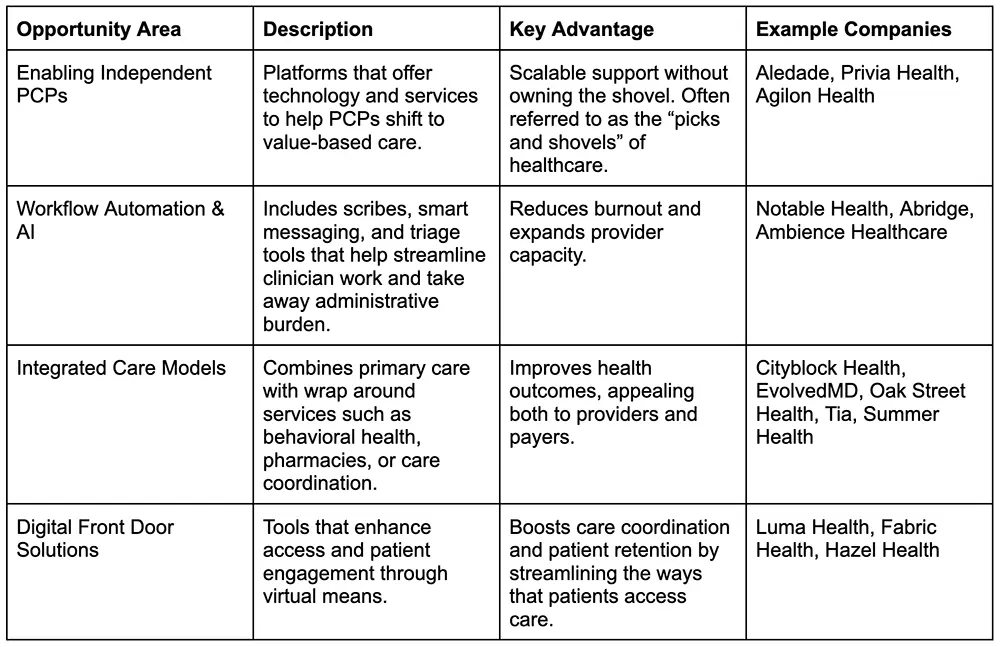

Where Innovation Still Holds Promise

Despite these high-profile setbacks, several areas within primary care still hold more defensible, scalable opportunities. Startups such as EvolvedMD, Tia, and Summer Health are providing highly focused, tech-enabled, and service-integrated models and are thriving by avoiding the heavy capital burden of legacy clinic-based models while still driving positive patient outcomes.

Backing the Backbone: A Smarter Bet on Primary Care

Given the persistent structural challenges—thin margins, workforce shortages, and a difficult reimbursement environment—we recommend against investing in direct primary care delivery startups at this time.

Instead, innovation should focus on infrastructure, tools, and enablement. Models that improve provider productivity, reduce cost of care delivery, or empower existing PCPs offer more promising returns and lower risk. Companies serving both primary and specialty care create broader go-to-market potential.

By investing in the scaffolding around primary care rather than in its direct delivery, venture capital firms can still help rebuild a high-functioning healthcare system.