Market Shifts and Cultural Forces

- Fertility is now mainstream: Once niche, fertility care is becoming central to health, workforce strategy, and modern family planning—driven by shifting societal norms, delayed parenthood, and greater visibility of diverse family structures.

- Cultural change meets tech innovation: From AI-driven nurse support to at-home IVF kits and employer-sponsored benefits, startups are democratizing access and affordability.

- Big gaps = big opportunity: Male infertility, postnatal loss, and inclusive care for LGBTQIA+ and BIPOC communities remain underserved, creating significant whitespace for innovation and impact.

- Market momentum is real: The fertility market is expected to reach $8.7B by 2033, with strong tailwinds from policy reform, CPT code expansion, and employer demand.

- Investor takeaway: Bet on clinically rigorous, culturally competent platforms with scalable infrastructure. The most successful companies will combine inclusivity, smart distribution, and medical excellence.

“You are past childbearing age.” Words that once pierced many individuals are now being reimagined with possibilities. Family dynamics are changing and along with that comes a new definition of what family planning means. In the past, raising a child often followed a particular mold: marriage, two-parent households, and heteronormative relationships. Anyone outside of this mold was excluded from the conversation.

Fertility is facing the opportunity to no longer be a niche solution. It is becoming central to how people live and plan their lives.

With the rise of employer-sponsored fertility benefits, the normalization of early egg freezing, tech-enabled diagnostics, and the proliferation of non-nuclear families, fertility services are undergoing a cultural and technological shift. We are excited by the wave of entrepreneurs rethinking how fertility care is delivered by focusing on affordability, transparency, and inclusive access.

In the United States, 1 in 5 married women experience infertility1. This has been historically driven by delayed parenthood planning and rising reproductive health issues. The reality of this phenomenon is moving to the forefront to normalize reproductive health experiences. For example, hit television shows like Harlem highlight the tremendous journey of egg freezing and the creation of chosen families, while public figures like Mindy Kaling and Chrissy Teigen have transparently shared their fertility journeys, illustrating that change is upon us. Now, the average age of first-time mothers has risen to 30 (up from 21 in the 1970s), and egg freezing cycles have grown nearly 400% in the past decade2. Additionally, LGBTQIA+ and single-parent households are driving demand for donor sperm, surrogacy, and reciprocal IVF.

Employers are also meeting the demand by expanding benefits to include fertility support. A now need-to-have for increased employee retention and satisfaction, reinforcing that fertility support is both a health and workforce imperative.

Market Size and Growth

The global fertility market is undergoing rapid expansion as it is projected to reach $8.7B by 2033. More than 10% of U.S. women have sought fertility services, and male infertility accounts for 50% of all infertility cases3. As access improves, particularly through employer-sponsored benefits and digital platforms, fertility care is becoming not only a personal health issue but an economic and societal one. Improving access can boost economic mobility for pregnant people and advance broader health equity. Importantly, this sector is now attracting the attention of likely acquirers such as Pharmacy Benefit Managers (PBMs), retail pharmacies (such as CVS and Walgreens), health plans, fertility clinic networks, and large employers seeking to enhance workforce benefits. Tailwinds such as the introduction of new CPT codes, expanded Medicaid waivers, and state-level reproductive health protections are also accelerating growth and reimbursement potential. These possibilities further highlight that fertility care is dynamic with a unique convergence of innovation, clinical need, and scalable impact.

Will Policy Emerge as a Driving Force in Fertility?

In February 2025, President Trump signed an executive order directing the development of policy recommendations to protect access to in vitro fertilization (IVF) and reduce associated costs. While this move signaled federal support for IVF, the executive order primarily called for recommendations rather than implementing immediate policy changes. As of now, the administration is reviewing these recommendations, but specific details and timelines for action remain undisclosed.

Bipartisan efforts like the Helping to Optimize Patients’ Experience (HOPE) with Fertility Services Act aim to mandate private insurance coverage for fertility treatments, including IVF. Similarly, the Right to IVF Act seeks to establish a statutory right to access fertility treatments and override conflicting state laws. However, these bills have faced obstacles in Congress, with some proposals being blocked despite public support for IVF access.

At the state level, responses vary. Louisiana passed legislation granting legal protections to IVF providers, aiming to prevent disruptions in services following legal uncertainties like those experienced in Alabama in 2024. Conversely, debates continue in other states regarding the ethical considerations and regulatory frameworks surrounding IVF.

As always, there are many unknowns to monitor closely:

- Federal Policy Implementation: The specifics of the Trump administration's forthcoming policy recommendations on IVF access and affordability, including potential regulatory changes or funding allocations.Legislative

- Progress: The advancement or stalling of federal bills like the HOPE Act and the Right to IVF Act, which could significantly impact insurance coverage and legal protections for fertility treatments.State-Level Legislation:

- Variations in state laws affecting IVF access, especially in states considering personhood definitions that could classify embryos as children, potentially complicating IVF procedures.

- Insurance Coverage Trends: Changes in insurance policies, both public and private, regarding coverage for fertility treatments, which could influence affordability and access for patients.

Technology and Innovation Landscape

The fertility landscape is undergoing a rapid transformation. Over the next decade, we expect meaningful shifts in treatment efficacy, affordability, and access—driven by innovation in care delivery models, AI-led decision support, and increased societal focus on inclusive family planning. As investors, we see a growing opportunity to back startups who can successfully lock access, affordability, and personalization in reproductive health.

Within the last five years, we have seen Kindbody, Maven, Carrot, and Frame rive change across the fertility care continuum. We continue to monitor closely as these companies pioneer what truly accessible and democratized access to fertility care looks like. We also see exciting potential in how payments solutions can tackle the high-cost barrier to fertility treatment, as seen in Progyny, Gaia, and Future Family. These companies are helping reduce the historically high cost of fertility treatment and improve the experience for patients traditionally priced out of care. These solutions also reflect a shift toward consumer-centric, vertically integrated care.

Despite growing demand, much of the fertility sector remains under-optimized. Embryologists and clinicians still rely heavily on manual assessments and legacy workflows in IVF labs. While AI-led embryo and sperm analysis tools are emerging, as seen through AIVF, they remain early-stage and require validation through larger prospective trials. Similarly, omics technology—beyond genetic testing—is underutilized in clinical workflows, presenting a significant white space for future platform companies.

Perhaps most limiting is the fertility sector’s data infrastructure. Patient-level data (e.g., hormone levels, ultrasound results, prior diagnoses, partner history) is fragmented across clinics, hospitals, and universities. This fragmentation limits personalization, reduces treatment efficacy, and slows the discovery of new biomarkers or therapeutic targets. Startups that solve for structured data aggregation, interoperability, and predictive analytics across Assisted Reproductive Technology (ART) will play a pivotal role in the sector’s next chapter.

Key Barriers and Unmet Needs

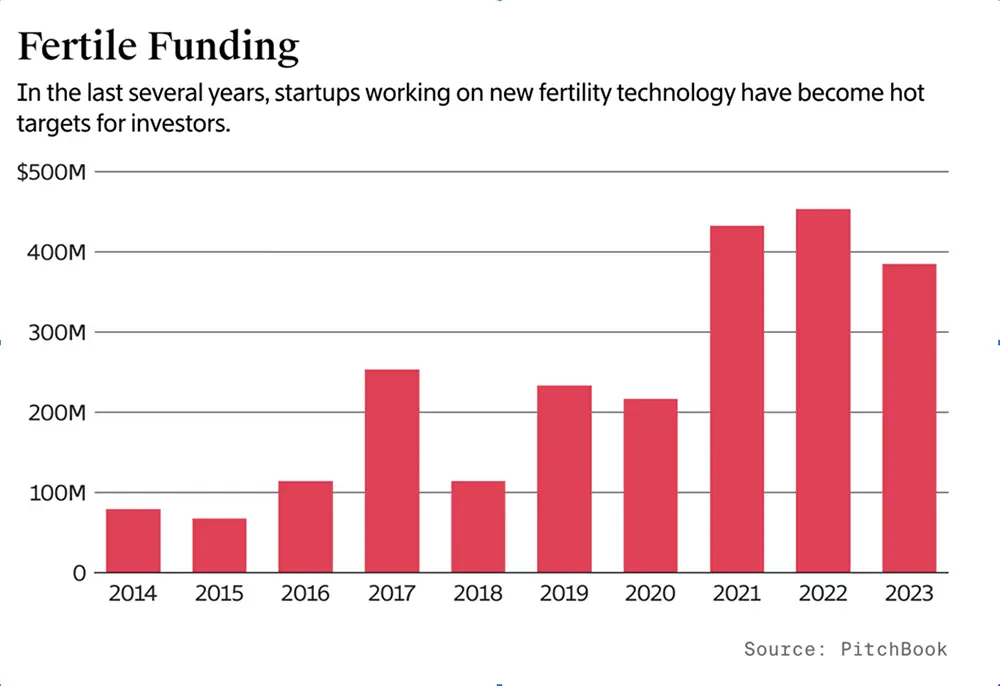

As investment into fertility startups grows—with $2.6B deployed between 2016 and mid-2021, though still far below other digital health sectors—significant white space remains.

The next generation of male infertility diagnostics, support for postnatal fertility loss, affordable at-home solutions, and payor-agnostic platforms that can guide patients regardless of insurance status are largely under-penetrated. Many startups also default to serving affluent, cisgender, heterosexual women, leaving behind LGBTQIA+ individuals, men, and lower-income populations. Black, Indigenous, and Latinx women face higher rates of infertility yet encounter the steepest barriers to care, including cost, geographic access, and provider bias.

Despite eight million IVF births since 1978, insurers still often view ART as niche or experimental. While 17 U.S. states mandate some form of infertility coverage, access varies widely. Without more universal reimbursement models, innovation will need to work around the payer—or redefine it altogether through employer and direct-to-consumer channels.

Looking Ahead: The Fertility Opportunity

Investors should prioritize startups that combine strong clinical foundations with inclusive, patient-centered design. Strong companies also build diverse provider networks and embed cultural competency into their care models to address the needs of LGBTQIA+ individuals, BIPOC communities, and nontraditional families. Key signals of readiness include distribution strategies that extend beyond employer-sponsored benefits to include telehealth platforms, payor partnerships, and direct-to-consumer channels. In a new age of technology, we place a heavy emphasis on companies with strong backend infrastructure: interoperable data systems, HIPAA-compliant privacy practices, and real-time outcomes tracking. These capabilities are powerful differentiators and value-creation levers that position companies for sustainable growth and the ability to truly transform the fertility space.